Deciding What Game You’re Actually Playing - Investing Objectives

Source: ChatGPT

Deciding What Game You're Actually Playing – Investing Objectives

What's your investing objective?

Most people answer with a return target: "10% annually" or "beat the S&P 500." But that's really not the first question to answer. Before deciding what you want to make, decide in what kind of game you can actually remain.

Most investors hunt for better returns - which makes sense – who wouldn't want bigger gains? But very few people stop to ask what their investments actually need to accomplish. That gap between searching and defining typically hurts investors more in the end than any market correction (but most will never realize that).

An investing objective doesn't predict the future. It sets boundaries and a target. It defines what you can tolerate, what you require, and what might cause you to abandon a plan at exactly the wrong moment. When objectives stay vague, strategies drift – and drift usually turns into poor decisions when markets get challenging.

Clear objectives don't guarantee success, but unclear ones almost always guarantee frustration.

The Three Non-Negotiables

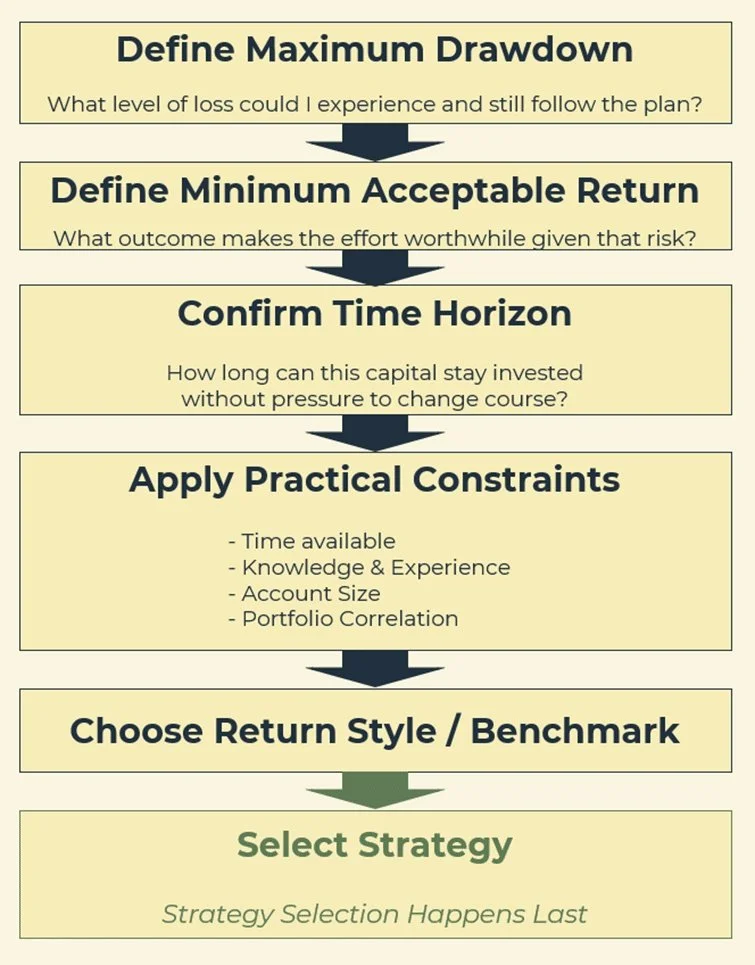

Every investing objective rests on three core factors. Ignore any one of them and the strategy eventually breaks down.

1. Maximum Drawdown

Maximum drawdown sets the deepest decline you can experience and still stick with the plan.

Always start here because this number matters more than expected return. Market behavior and personal discipline tend to fail first, not the math.

Many investors believe they tolerate larger losses than they actually do – especially when an enticing return comes attached to the strategy. When a portfolio drops 25–30%, even experienced professionals find their resolve tested in real time. For most people – and this holds true with many professional managers – 10-15% marks the red line. If you abandon the strategy during the drawdown, the strategy failed - even if it later recovers.

The drawdown establishes emotional and financial guardrails.

2. Desired Return

Return goals need realism, not optimism. Higher returns typically come with greater variability. That relationship practically never disappears, even when markets run hot.

A useful return objective focuses less on hitting an impressive number and more on answering a simpler question: What outcome makes this effort worthwhile, given the risk taken?

Return and drawdown must align. When they don't, fear or frustration usually follows.

3. Time Horizon

Time horizon defines how long capital can remain invested without interruption. Long horizons allow recovery from setbacks. Short horizons demand tighter controls and closer management.

Many people invest as if they won't need the money for years, but real life often proves otherwise. When that happens, the original plan no longer fits and will need to be revised.

Time horizon quietly eliminates many strategies before investors realize it.

Here's the catch: You can optimize one or two of those variables – but not all three at once. Tradeoffs come with the process.

Additional Constraints That Quietly Matter

Beyond the big three, several practical constraints shape what works in real life.

Capital Size – Some strategies function poorly at smaller account sizes. Costs, diversification limits, and position sizing all matter.

Knowledge and Experience – Some approaches demand judgment, monitoring, and emotional control. Others reward simplicity. Complexity only helps when skill supports it.

Time Available – Any strategy or system requires upkeep. Rebalancing, rule-following, and monitoring all consume attention. A plan that asks for more time than you can give eventually breaks down.

Correlation With Other Investments – Investments that moves in lockstep with everything else likely add little protection or better returns. Diversification only helps when different investments behave differently under stress.

These constraints reflect reality, not abilities. They help filter viable options.

Choosing the Return Style That Fits

When objectives and constraints come together, they naturally point toward one of three broad return styles:

Absolute Return – The goal focuses on producing gains regardless of market direction. Risk control matters more than participation. These approaches often emphasize drawdown limits and low correlation. Active management and discipline carry significant weight for this style. (The SmartSignal System exemplifies this return style.)

Benchmark-Beating Return – The goal involves outperforming a specific market index. This approach accepts periods of underperformance and tracking error. A system with a multi-cycle track record, conviction, and patience all become essential.

Benchmark-Matching Return – The goal centers on capturing market returns efficiently and consistently. Simplicity and cost control dominate. If the benchmark declines, your investment will likely decline as well. Time and diversification do most of the work. This return style generally requires the least management and can very well be passive.

None of these approaches ranks as "better." Alignment with your objectives and “who you are” determines success.

Choosing the Right Benchmark

Benchmarks provide context, not motivation.

A useful benchmark matches asset class, volatility, and time horizon. Poor benchmarks distort expectations and create false confidence or unnecessary disappointment.

The benchmark's job involves measurement, not pressure.

Getting the Order Right

Investors often struggle not because the decisions feel difficult, but because they approach them in the wrong order. Ever fall in love with an investment because the return number looked attractive? Most of us have. But when we put return goals first, we end up trying to bend everything else to justify that number.

A better approach reverses that logic -

Source: Author

One Question That Helps Clarify Strategy Selection

At times, a strategy or system will outperform its historical averages. At others, it will underperform those measures. That's natural and expected. For longer-term systems, those periods might stretch many months or even a few years.

Before committing to any longer-term strategy, ask this:

If this approach stays within its risk limits but disappoints for many months (10-24?), would I still follow it?

If the answer feels uncertain, the objective and selection process probably needs more work.

The Real Goal

Investing works best when objectives lead and strategies follow. Clear boundaries reduce emotional decisions and allow systems to operate, especially when markets turn uncomfortable.

The goal never involves predicting outcomes. The goal involves choosing a game you can win – and more importantly, one you can stay in long enough for that to happen. In the end, the best strategy isn't the one with the highest theoretical return; it's the one you'll actually follow when markets test your resolve.

Worth considering: This framework works for what you already own, not just new investments. Most investors accumulate a portfolio over time without testing older investments against clear objectives.

Time for a review?

+++++++++++++++++

To receive helpful information for self-directed investors within 10-15 years of retiring, click here for our free weekly newsletter.

Important Disclosures

Past performance does not guarantee future results. Investing involves risk including the possible loss of principal.

The performance shown combines two different kinds of data. Results from January 2003 through December 2024 reflect backtested application of the SmartSignal methodology to historical price data. Results after January 2025 reflect actual signals delivered to subscribers during that period.

Backtested performance has inherent limitations. It does not represent actual trading. Backtested results benefit from hindsight and do not reflect the impact of trading costs, execution slippage, market liquidity, or the psychological pressures of investing real money during live conditions. For these reasons, backtested performance may differ materially from actual results. Individual subscriber results may also vary based on execution timing, account composition, and other factors.

TenHundred Co., its officers, employees, and partners may hold positions in the ETFs or securities referenced by the SmartSignal methodology, and may trade those positions without notice. TenHundred Co. reserves the right to modify or discontinue the methodology at any time, and past performance data may not reflect the current methodology.

Growth Guardian Investor publishes systematic investing education and methodology training under the publisher's exclusion to the Investment Advisers Act of 1940. We do not provide personalized investment advice. Subscribers make their own investment decisions.

Full Disclaimers Statement on www.gginvestor.com.