Prepare for the Bear: How to Protect What You’ve Built

It’s two in the morning.

Imagine that somewhere, an investor checks their phone and sees overnight index futures dropping like a rock – down hundreds of points.

Sleep’s gone. Their mind races: “Should I sell? Should I do something?”

I understand that feeling – the uncertainty, the fear of making the wrong move – because that was me. I didn’t have a process to handle moments like that.

In 1998 and 1999, I sat out the raging dot-com bull market completely, convinced a bear market was just around the corner. Eventually, the decline came – but I missed out on gains for two full years. Then, I had no plan to get back in and missed gains again.

By 2006 to 2008, I was trading short-term in a cash account but still didn’t have a framework for investing my retirement money. When the market took off again in 2009, I missed that opportunity too.

That has all changed. Today, I follow a systematic process – a written set of rules that keeps me invested during late-stage bull markets and helps me be ready when the next bear begins.

If you’re managing your own money, you can do the same. Preparation, not prediction, separates those who survive market cycles from those who panic at the wrong moment.

Why Preparation Matters

What worries me isn’t the market cycle. The market always moves through phases – up, down, and sideways. That’s just what markets do.

I worry about the many investors who have been riding this bull market for ten years or longer without a plan for what’s coming up.

We have had a record-breaking bull run. History suggests that the following bear may match the bull’s run. Every major decline eventually recovers – but sometimes that recovery takes a decade or more. If you’re near retirement, a ten-year rebound can collide directly with your income window.

The difference between those who make it through with their accounts intact and those who don’t isn’t intelligence or luck – it’s preparation.

1) Start With a Simple Written Plan

When prices fall fast, adrenalin fueled emotions takes over. A written plan, drafted when you feel calm, becomes your lifeline when fear sets in.

A very basic plan needs to answer three questions:

1. What future are you funding – and when?

Living expenses, travel, helping your kids, etc.

Make these real – first what you need, then what you’d like.

How much for each?

When? (5 years vs 15 years changes everything).

2. What level of loss would make you want to abandon your plan?

Be honest. That number defines how much risk your portfolio should carry.

Start by recalling how much your portfolio has declined in the past and how you reacted.

3. What rules will you follow when markets change?

Decide how often to rebalance,

When to add cash,

Under what conditions to reduce exposure.

Write these down!

It’s not a full financial plan by any stretch, but those answers transform uncertainty into clarity. They can guide your actions when emotions tempt you to react impulsively.

And if you prefer not to design it yourself, a fee-only advisor can help you craft a plan that still lets you stay in control.

2) Diversify for Stability

Many investors believe they’re diversified because they own both small-cap and large-cap stocks. In reality, that’s just a lot of stocks – and when bear markets hit, they all fall together. True diversification blends assets that don’t move in sync: bonds, gold, commodities, even cash.

This kind of balance doesn’t chase the highest return – it preserves behavioral stability, helping you stay invested long enough for compounding to keep working.

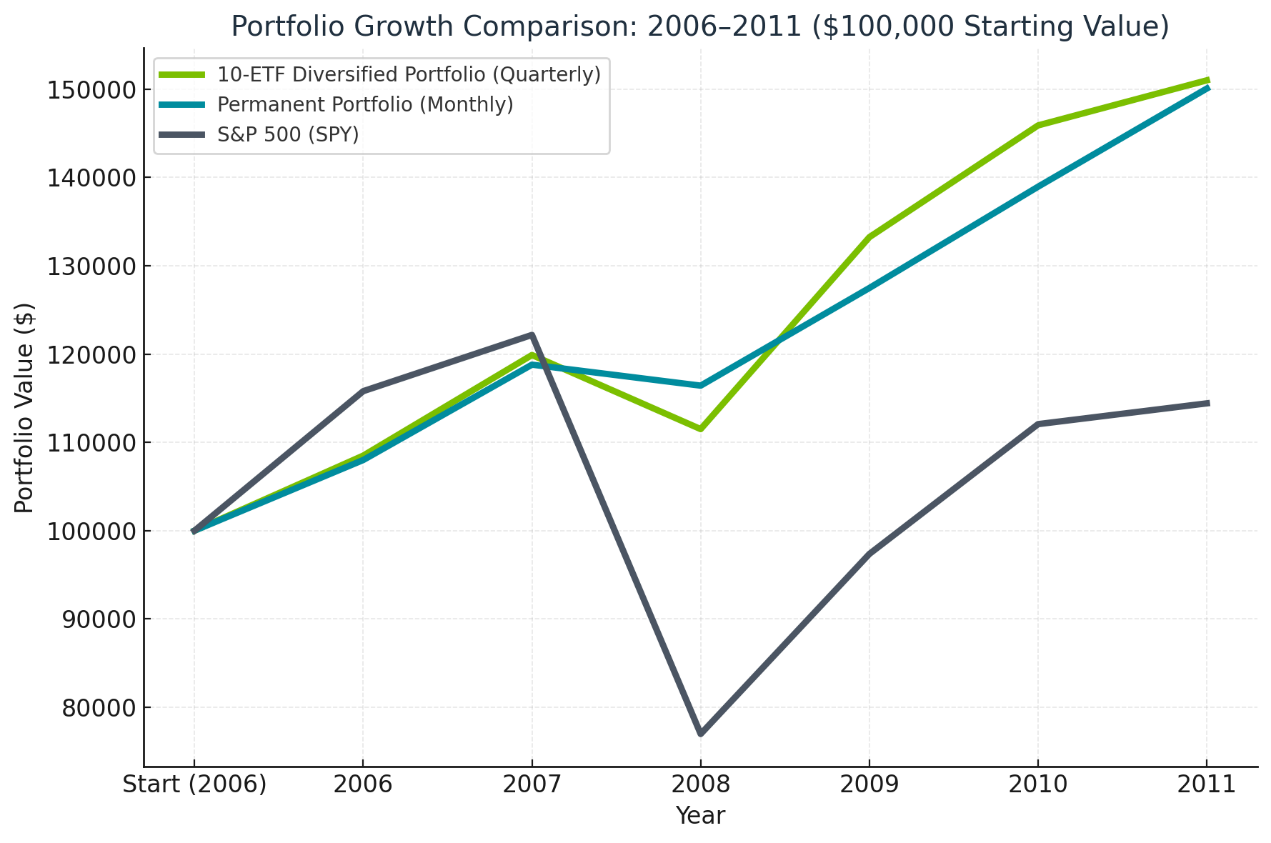

Data from past downturns shows how effective diversification can be. During the last two major bear markets, stock-only portfolios dropped more than 50 percent, while well diversified portfolios fell much less – anywhere from 10 to 25 percent. Here are examples of how two diversified portfolios fared in the global financial crisis

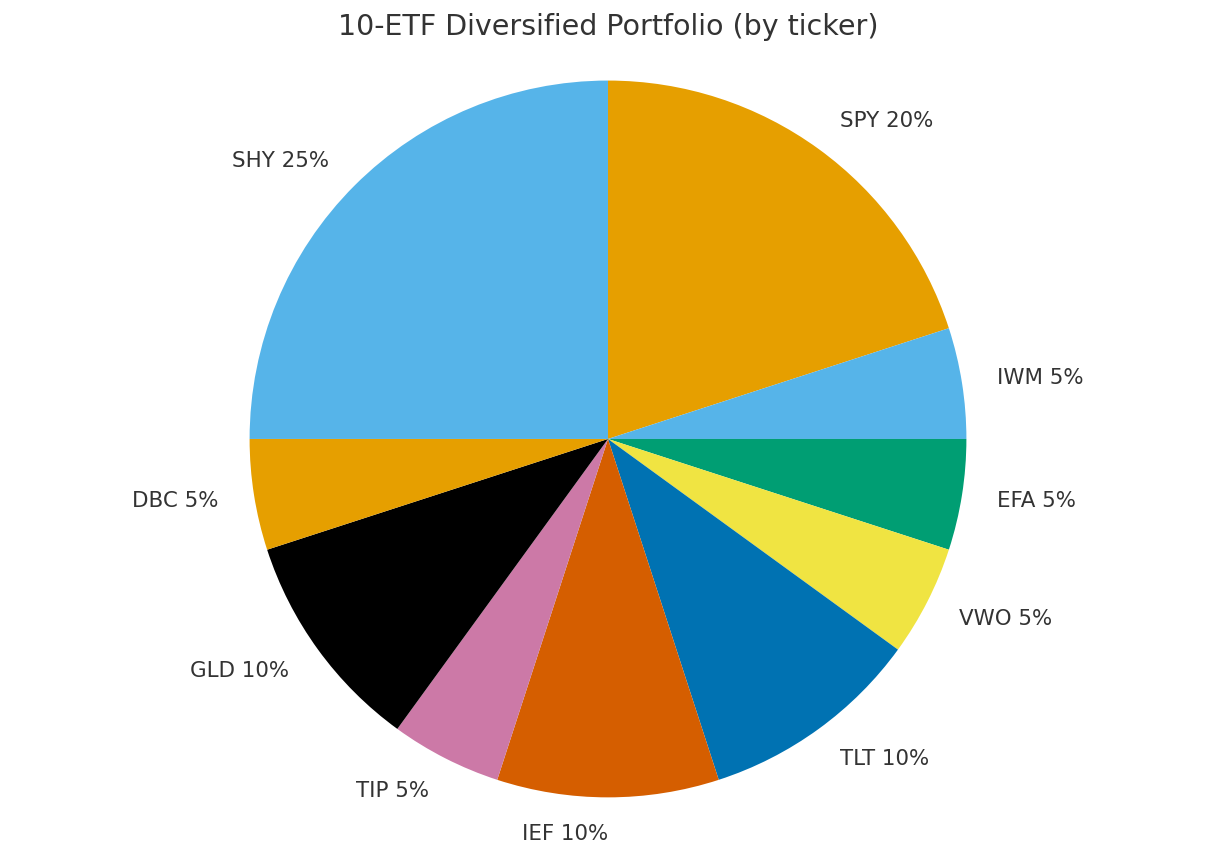

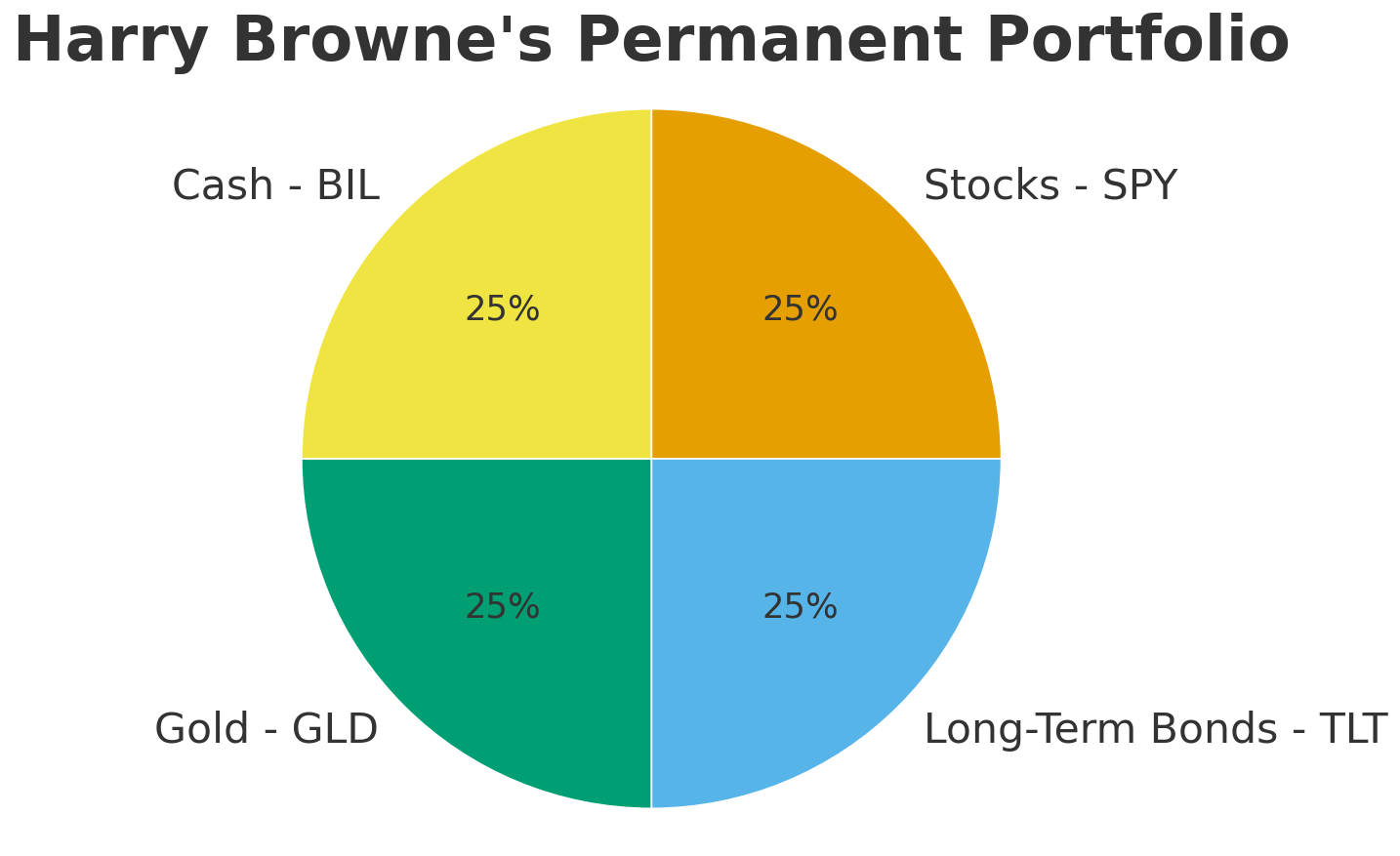

One diversified model uses ten ETFs across multiple asset classes, with roughly a third in equities. The other, Harry Browne’s Permanent Portfolio, uses only four assets – stocks, long-term bonds, gold, and cash – and yet it performs surprisingly well.

The point isn’t to try and create the perfect mix. It’s to understand that diversification acts as shock absorption for your emotions as much as for your balance sheet.

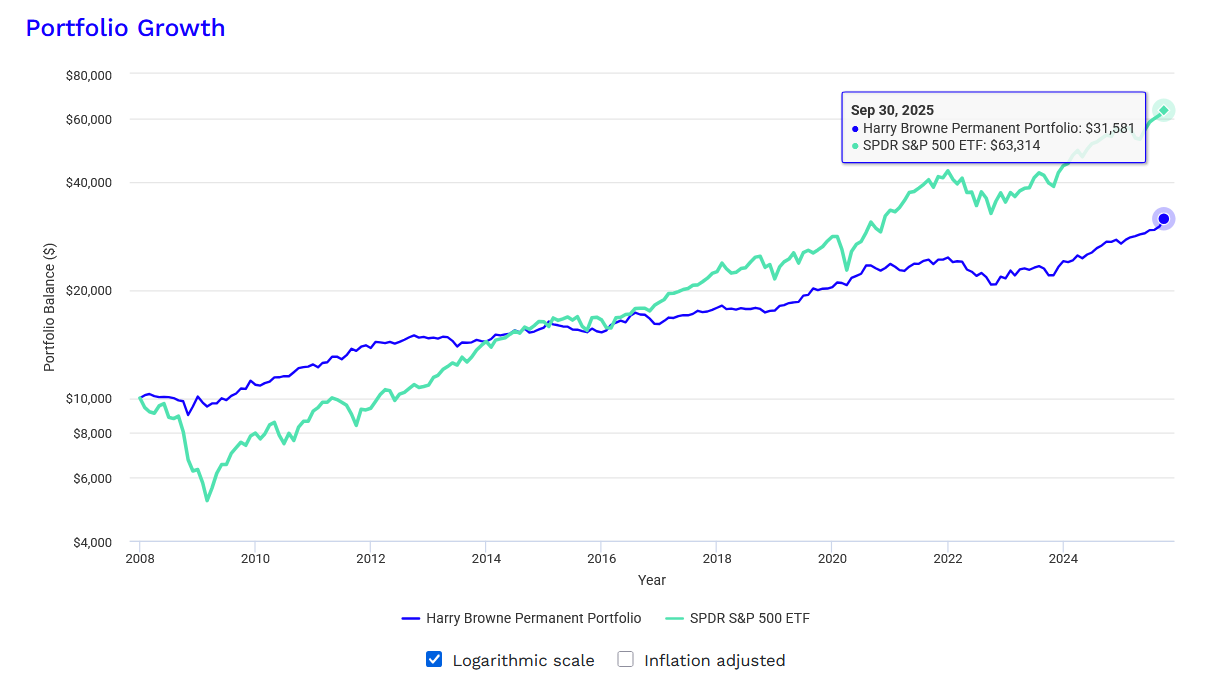

Diversification cushions declines but often lags during strong bull markets. That’s the trade-off of staying invested long term in diversified portfolios: steadier results, slower surges.

any investors remain diversified forever, and that’s fine – it keeps them steady through storms. A systematic approach to diversification can go further where you increase diversification during late-stage bulls for safety and then concentrate more in stocks when a new bull begins for growth.

That requires structure, discipline, and a plan – not prediction, but preparation

3) Use Cash Intentionally

Cash often gets dismissed because it lags inflation, but cash buys something more valuable: psychological safety.

In 2000 and 2008, investors who kept solid cash reserves slept better at night. When markets began recovering, they had dry powder to invest in the deals available on most stocks.

How much?

If you’re far from retirement, consider holding 10–20 percent in cash.

Within five to ten years of retirement, aim for 20–30 percent.

At the very least, hold one year’s living expenses in cash once you’re retired.

Knowing your bills are covered changes how you handle volatility when it arrives.

Cash doesn’t just defend – it also lets you go on offense. When the market sells off, great companies trade at 40–50 percent discounts – but you can’t buy bargains easily if you don’t have cash ready.

4) Add a Rules-Based Active Management Layer

Some investors want to go beyond static defense. They use rules-based systems that adjust market exposure based on objective measures of strength or weakness.

These systems are risk-on when trends are strong and risk-off when momentum fades. They rely on data – price trends, relative strength, volatility – not gut or feelings.

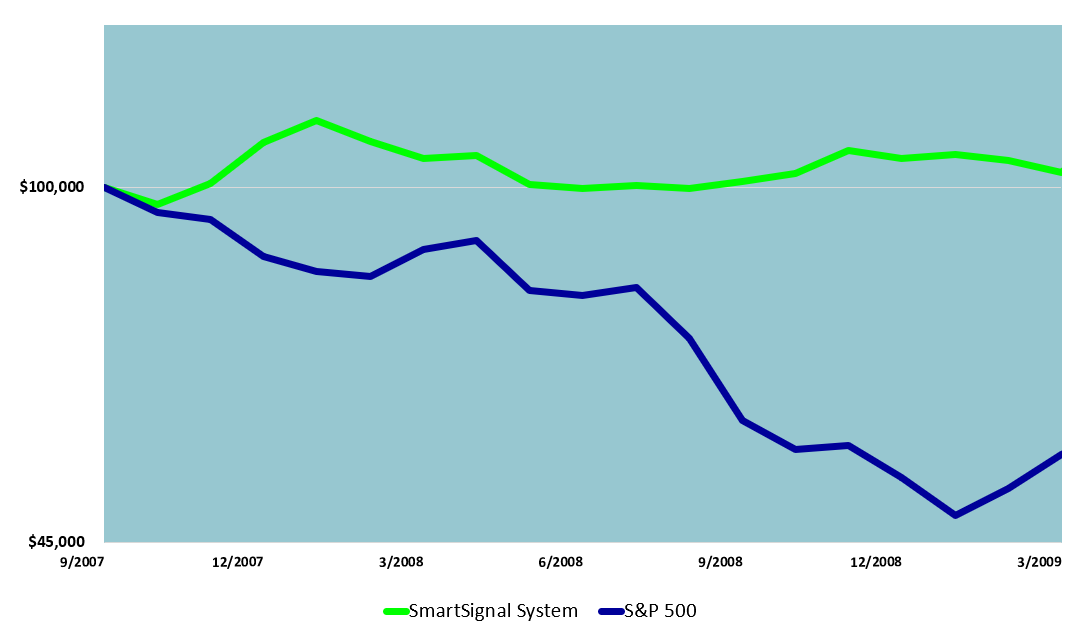

In 2008, systematic approaches like these reduced losses dramatically while some even turned small gains as the market fell 56 percent. In long bull markets, they stay invested without second-guessing every headline. Note: past performance does not imply future performance.

You can build your own process or follow a proven model, but the principle stays the same:

Prepare for market shifts through structure and process, not emotion or intuition.

You don’t need to outsmart the market – you need to stay aligned with it.

Confidence Through the Cycle

Two major bear markets taught me an important lesson: fear fades when you have structure.

A written plan to steady your mind and clarify your next move.

Diversification to cushion the hit when one area struggles.

Cash to preserve the freedom to stay calm and act deliberately.

And for some, an adaptive system to play both defense and offense systematically.

Together, these form a framework for any market season – bull, bear, or sideways.

Your Next Step

Before the weekend, choose one action.

Write your rules. Rebalance your mix. Set aside some real cash.

Small steps now prevent big regrets later. The time to prepare isn’t when the sky has turned dark – it’s while the sun still shines and you can think clearly.

Preparation and process changed everything for me. They reduced my worry and helped me act with confidence instead of emotion – staying invested through the full bull phase, moving to safety when the bear arrives, and moving again to being invested when conditions improve.

That’s what I want for you – calm confidence through the full market cycle, the kind that lets you take a 2am glance at headlines but be able to get back to sleep knowing you have a plan.

Guard what you’ve built. Grow what you have.

+++++++++++++++++

Important Disclosures

Past performance does not guarantee future results. Investing involves risk including the possible loss of principal.

The performance shown combines two different kinds of data. Results from January 2003 through December 2024 reflect backtested application of the SmartSignal methodology to historical price data. Results after January 2025 reflect actual signals delivered to subscribers during that period.

Backtested performance has inherent limitations. It does not represent actual trading. Backtested results benefit from hindsight and do not reflect the impact of trading costs, execution slippage, market liquidity, or the psychological pressures of investing real money during live conditions. For these reasons, backtested performance may differ materially from actual results. Individual subscriber results may also vary based on execution timing, account composition, and other factors.

TenHundred Co., its officers, employees, and partners may hold positions in the ETFs or securities referenced by the SmartSignal methodology, and may trade those positions without notice. TenHundred Co. reserves the right to modify or discontinue the methodology at any time, and past performance data may not reflect the current methodology.

Growth Guardian Investor publishes systematic investing education and methodology training under the publisher's exclusion to the Investment Advisers Act of 1940. We do not provide personalized investment advice. Subscribers make their own investment decisions.

Full Disclaimers Statement on www.gginvestor.com.