Drawdowns Destroy Compounding

Most investors obsess over returns. The smart money obsesses over drawdowns.

Here's a reality that catches most investors off guard: a 55-year-old with $500,000 who avoids just one major drawdown could retire with $200,000 more. Not from timing five perfect investments or making 10 lucky calls. Just one avoided drawdown. Here's what nobody tells you about compounding - the math only works if you minimize declines.

Drawdown Math

Let me show you.

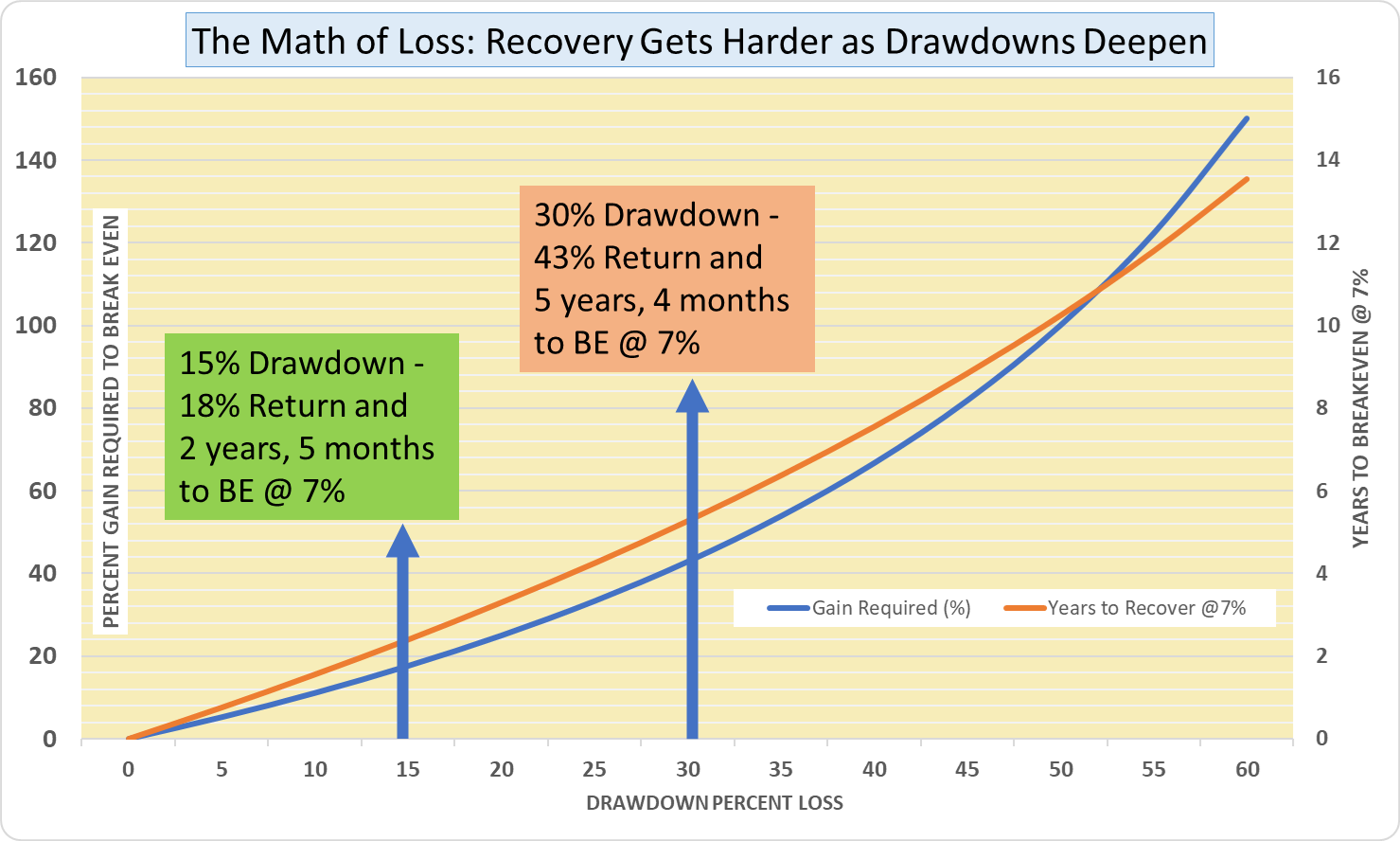

When you lose 30%, you need a 43% gain just to get back to breakeven. Lose 15%, and you only need an 18% gain. That difference compounds brutally over time. At a 7% annual return, recovering from a 30% loss takes more than five years. Recovering from a 15% loss? About two and a half years.

Twice as much recovery time for a larger loss when you can least afford it – just when time is getting shorter. And it’s not compounding time - that's recovery time, getting back just to where you started before the drawdown. For someone who's 60, that difference could mean working until you pass your 66th birthday instead of retiring before you turn 63. Same starting point, same discipline, different drawdown.

Two Volatility Gremlins

Ed Easterling runs Crestmont Research from a small Oregon town, but his math explains Wall Street concepts better than most Manhattan analysts. He identified what he calls volatility gremlins - two hidden ways that choppy markets destroy wealth.

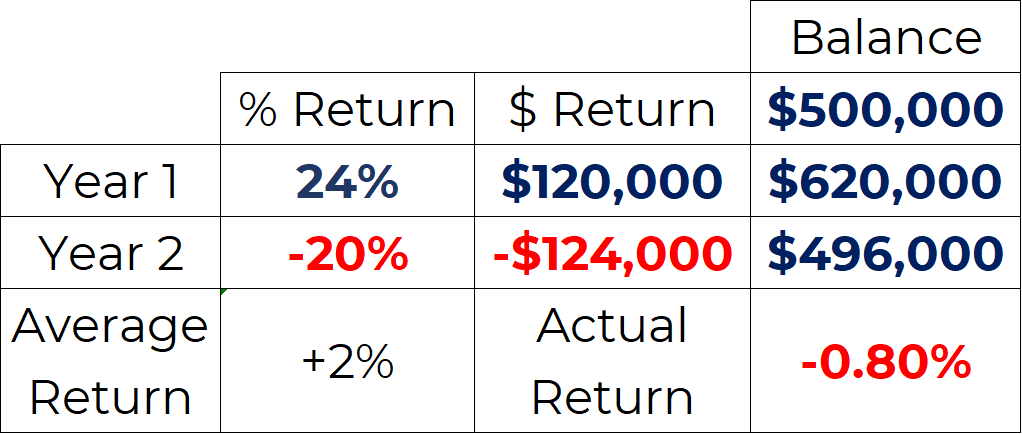

The first gremlin is asymmetry. If you're up 24% one year and down 20% the next, you don't average 2% over two years. You actually lose about 1%. That math isn't intuitive, but it's absolute.

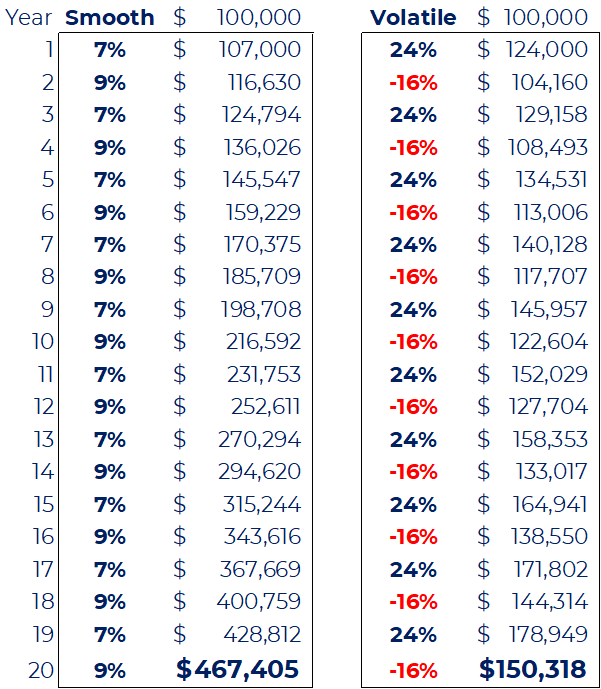

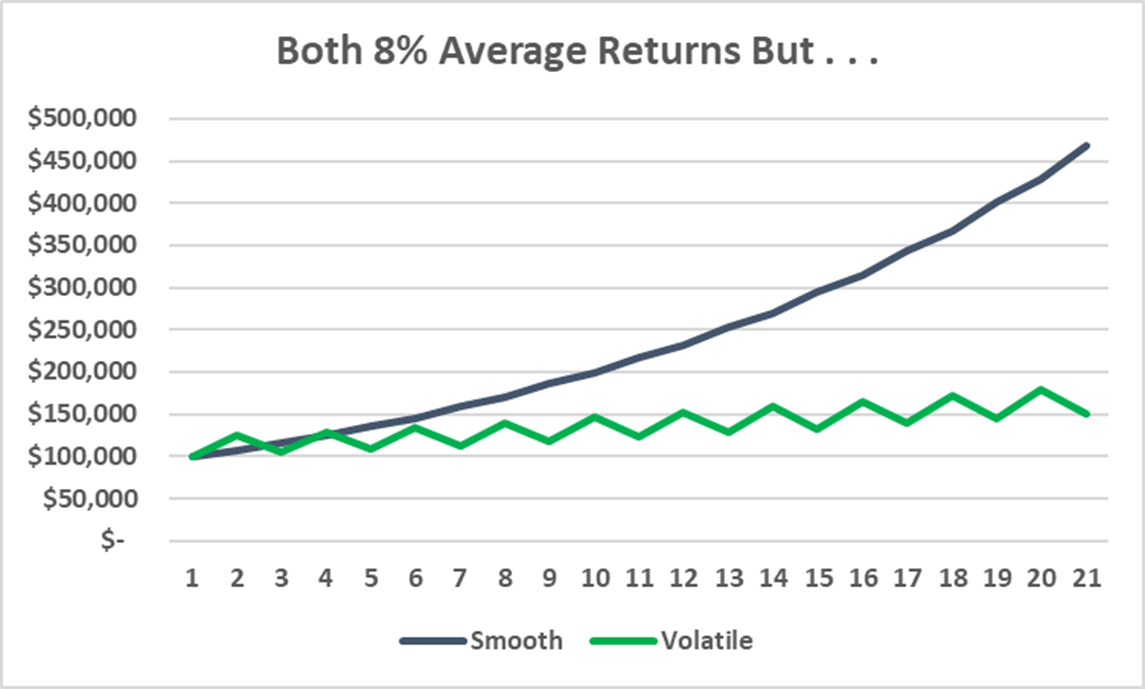

The second gremlin is return dispersion. Take two portfolios with the same 8% average annual return over 20 years. Portfolio A is pretty steady, earning 7% and 9% in alternate years. Portfolio B swings wildly - up 24%, then down 16%, repeatedly. Same average return, but very different endings. The smooth portfolio ends about three times higher. Why? Because volatility is a math tax. Every big swing down erases more than the next swing up can recover.

You might think compounding doesn't matter anymore in your mid-fifties or early sixties. Not so, Joe. Odds are you still have 20 to 30 years ahead of you. That's plenty of time for compounding to work its miracle, or plenty of time for volatility to wreck it.

That 20-to-30-year window includes one particularly vulnerable stretch - a decade when drawdowns inflict maximum damage.

Red Zone

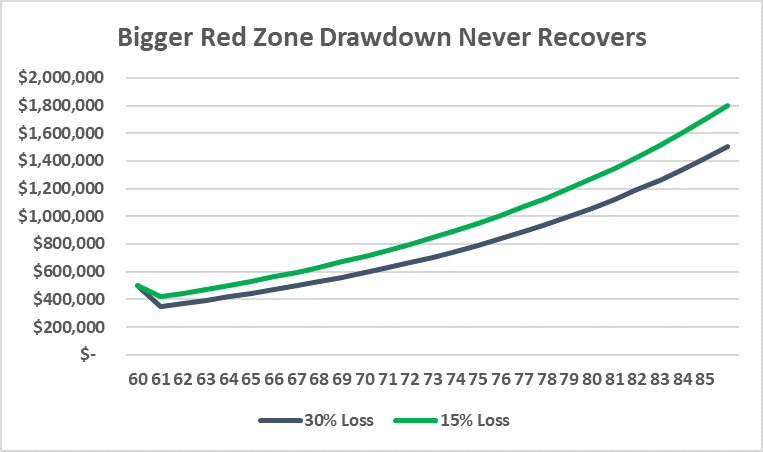

Financial planners call the period five years before and five years after retirement the retirement red zone. This is when drawdowns do maximum damage because you're shifting from accumulation to distribution.

Picture two people, both 65, both with $500,000. One experiences a 30% drawdown early in retirement. The other has only a 15% drawdown. By age 75, the difference might be $150,000. By 85, it could be $300,000 or more. Same starting point, vastly different retirement security.

The Hidden Advantage to Limiting Drawdowns

The investor who limits drawdowns isn't just protecting their wealth - they're preserving their ability to act. When opportunities appear, like March 2009, an investor down 15% could lean in and add capital. The investor down 40%? Frozen, scared, sidelined during one of the best buying opportunities in decades.

The dollar loss might not even be the worst part. The behavioral damage could be worse. When fear takes over, many investors sell at the worst possible time. Studies show that large drawdowns cause investors to abandon their strategy entirely - the entire plan, not just a position or two.

A 15% decline? Most people can handle that. They stay invested. A 35% or 45% decline? That breaks people; they panic. Research shows they often never come back. They sell, lock in their loss, then stay in cash for years, missing the most of the market recovery.

Protecting Compounding

First, don’t try predicting crashes. Instead, prepare your portfolio for bigger declines - ahead of time.

Picture two investors back in 2007, both 60, both with half a million dollars. When the financial crisis hit, Investor A had already prepared systematically:

Investor A kept a 12-month cash reserve - one year of living expenses in cash and short-term treasuries. When the market crashed, they didn't panic or need to sell near the bottom. That cash cushion gave them calm and flexibility.

Investor A also diversified across asset classes - not just large caps and small caps, but other assets that responded differently to growth, inflation, and interest rates. Different engines for different weather.

Finally, Investor A used a systematic risk management process. Not gut feeling, not reacting to headlines - a disciplined system that monitored conditions and adjusted position sizes when risk rose.

The result? Investor A retired in 2012 at age 65 with a good sense of financial security. Investor B did manage to hold on through the worst of the decline, stayed shaken for a few years, and then had to keep working until 69 in 2016. Now, that's not exactly horrible, but it stands in sharp contrast to Investor A's position - retiring with both options and the confidence that comes from navigating a crisis successfully.

This type of outcome - having real flexibility and psychological confidence - drives the core philosophy behind the SmartSignal System. By focusing on capital preservation during major market drawdowns while participating when the market rises, the system aims to create more "Investor A" experiences and fewer "Investor B" outcomes

Compounding, The Quiet Miracle

Compounding converts discipline into wealth over decades. But it's fragile. You have to support it, because unsupported, the market will damage it. We can't predict when the next major drawdown hits - markets do what they do on their own schedule.

We can, however, prepare.

· Monitor the market cycle.

· Diversify across strategies and asset classes.

· Protect your behavior using rule-based systems.

Real wealth builders aren't focused on capturing every last percentage in a rally. They focus on controlling the damage when markets eventually fall.

Protect the curve, and it will protect you.